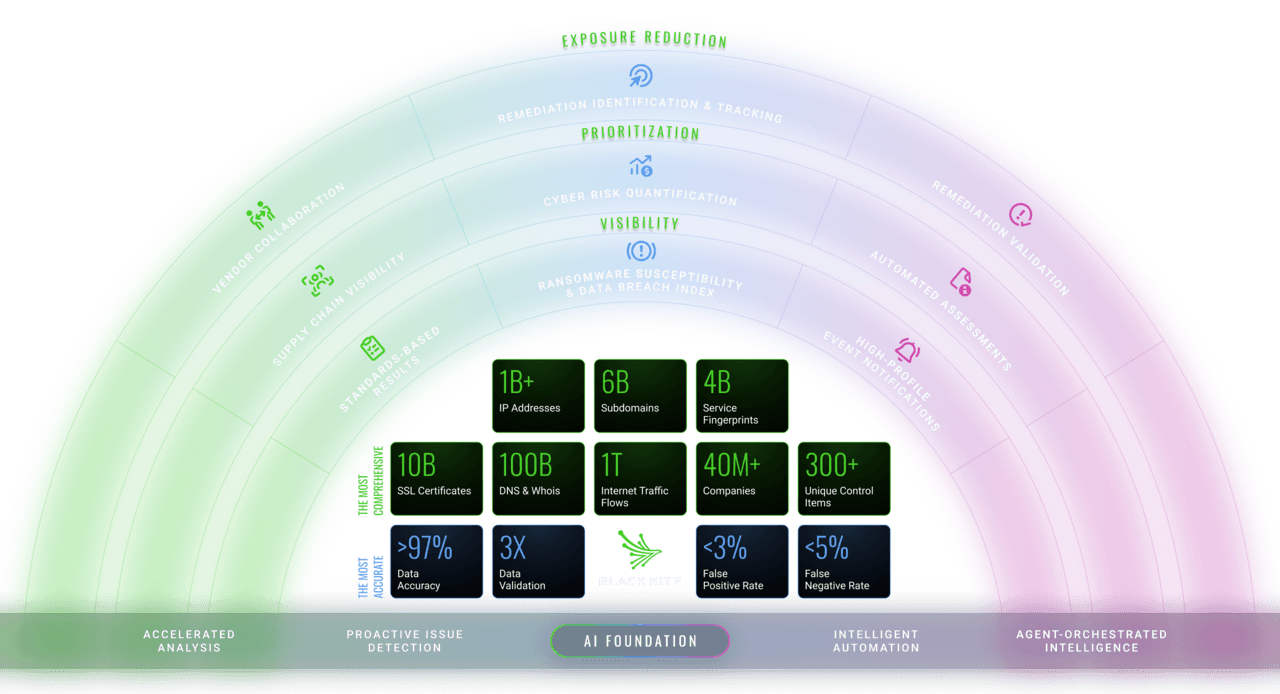

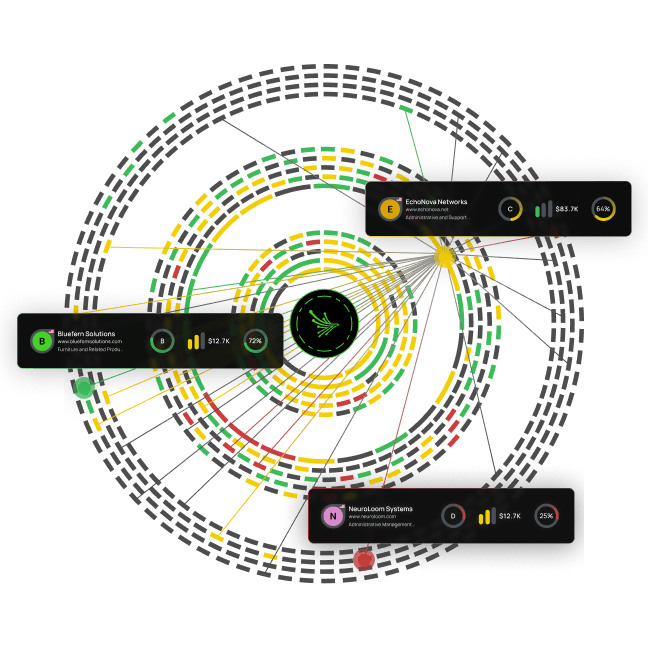

THIRD-PARTY RISK MANAGEMENT

Annual reviews and opaque scores weren't built for ecosystems that change daily. Black Kite gives TPCRM programs continuous visibility, open standards-based cyber ratings, and collaborative remediation tools that move beyond compliance theater into genuine risk governance.